The credit score range and categories play a significant role in determining an individual’s creditworthiness for different financial products, including Personal Loans. Having a clear understanding of these ranges and categories can provide valuable insights into one’s financial standing and enable informed decisions when applying for credit. Financial institutions, including NBFCs, acknowledge the importance of credit scores and strive to provide clarity on this subject. In this guest post, we will explore the credit score range and categories, including the CIBIL Score range for Personal Loans, and discuss the availability to check free CIBIL Scores.

Credit Score Range

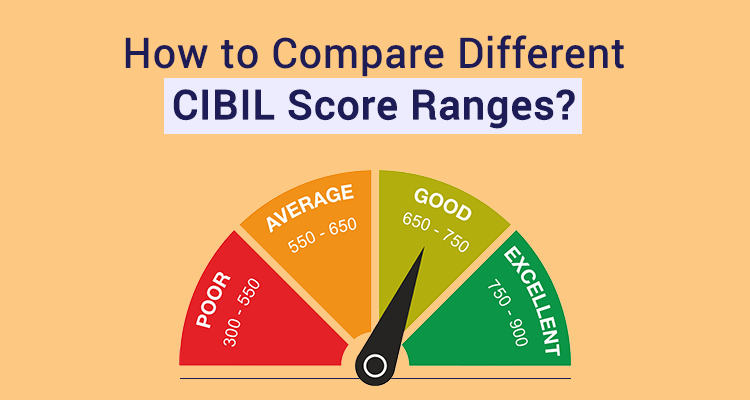

CIBIL Score range for Personal Loans is typically from 300 to 900, with higher scores indicating stronger creditworthiness.

Excellent (750-900)

An excellent credit score falls within the range of 750 to 900. Individuals in this category have demonstrated exceptional credit management and are perceived as low-risk borrowers. Lenders, including NBFCs, are inclined to offer favourable terms, competitive interest rates, and higher credit limits to those with excellent credit scores. Personal Loan applicants with scores in this range are likely to have a higher chance of approval from reputable financial institutions.

Good (700-749)

A good credit score ranges from 700 to 749. Individuals in this category have displayed responsible credit behaviour and have a solid credit history. While they may not enjoy all the benefits of those with excellent scores, they are still considered low-risk borrowers. Personal Loan applicants with good credit scores can expect competitive interest rates and favourable loan terms.

Fair (650-699)

A fair credit score falls within the range of 650 to 699. Individuals in this category have an average credit history but may have encountered occasional financial challenges. While they may still be eligible for Personal Loans, they might face slightly higher interest rates and stricter terms compared to those with higher scores.

Poor (550-649)

A credit score falling within the 550 to 649 range signifies lower creditworthiness. Individuals in this category may have experienced significant credit issues such as overdue payments, defaults, or high credit utilization. Getting approved for a Personal Loan with a poor credit score can be challenging, as financial institutions, including NBFCs or other lenders, perceive borrowers in this range as higher risk. If approved, the interest rates and terms offered may be less favourable. However, these lenders understand that financial situations can change and may offer suitable solutions for borrowers with less-than-ideal credit scores.

Very Poor (300-549)

An extremely poor credit score falls between 300 and 549. Individuals in this category have a history of severe credit problems, such as multiple defaults, bankruptcies, or delinquencies. Getting a Personal Loan with a poor credit score can be extremely difficult, as lenders may be hesitant to extend credit. In such cases, borrowers may need to explore alternative financing options or work on improving their credit before applying for a loan.

Availability of Checking Free CIBIL Scores

CIBIL scores, provided by the Credit Information Bureau (India) Limited, are widely used by lenders to assess creditworthiness. While platforms offer access to CIBIL scores, obtaining your CIBIL score directly from the official CIBIL website is recommended. The website allows individuals to access their credit scores and reports for a nominal fee. However, it is important to note that free CIBIL Scores may be available during promotional periods or as part of certain credit education initiatives.

Conclusion

Understanding the credit score range and categories is essential for evaluating one’s creditworthiness and making informed financial decisions. Whether an individual has an excellent, good, fair, poor, or extremely poor credit score, it is important to recognize that creditworthiness is not static and can be improved over time with responsible financial behaviour. Financial institutions, including NBFCs or other lenders, understand the significance of credit scores in the lending process and strive to provide suitable solutions for individuals across various credit score categories.

Regularly monitoring your credit score and taking steps to maintain or improve it can enhance the chances of securing favourable loan terms and financial opportunities. It is important to remember that a credit score is just one aspect of an individual’s overall financial profile, and lenders consider multiple factors when evaluating Personal Loan applications.